Executive Summary

The US manufacturing sector faces significant challenges, as indicated by the latest Institute for Supply Management (ISM) report. Key points include:

· Manufacturing PMI at 47.2 in August 2024, indicating contraction

· Declining new orders and production, reflecting weak demand

· Impact of higher interest rates on borrowing costs and investment

· Supply chain and inventory mismatches

· Ongoing challenges with purchasing costs despite easing inflation pressures

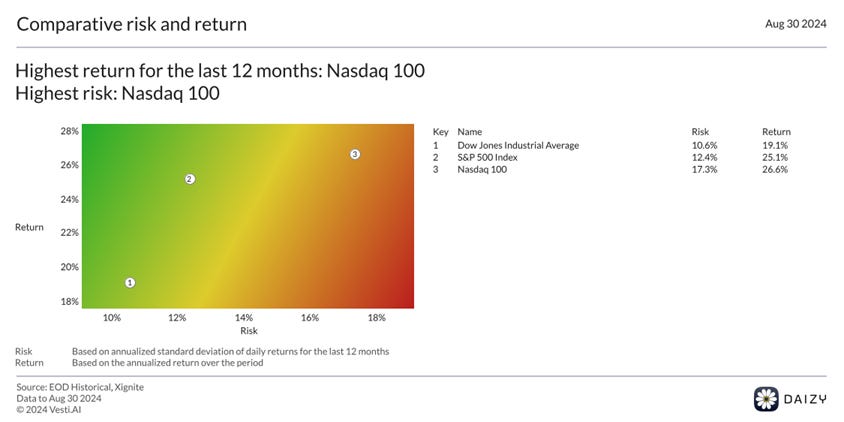

Despite these weaknesses, the Dow Jones Industrial Average (DJI) has shown resilience, returning 19.13% over the past 12 months.

September 3rd ISM report

The US manufacturing sector has been grappling with numerous challenges over recent months, as highlighted by various data points and reports. The latest Institute for Supply Management (ISM) report, released on September 3, 2024, provides a comprehensive overview of the sector's current state. This article will explore these weaknesses and assess their interconnected impacts on purchasing costs and the broader economic landscape.

Key Weaknesses and Challenges

Contracting Manufacturing Activity

The ISM report reveals that the Manufacturing PMI stood at 47.2 in August 2024, signaling contraction as it remains below the growth threshold of 50. This marks a continuation of a downward trend in manufacturing activity. The report highlights declines in new orders and production sub-indexes, signifying weak demand and subdued economic activity.

Slowing Demand and Economic Uncertainty

The manufacturing sector has been affected by weak demand and economic uncertainty. This has resulted in a decline in new orders and backlogs, with manufacturers expressing concerns about the outlook for Q3 2024. Economic uncertainty, driven by high inflation, rising interest rates, and the upcoming presidential election, continues to impact customer spending and business investment (Yahoo Finance, Sept 3, 2024).

Impact of Higher Interest Rates

Higher interest rates have posed challenges for the manufacturing sector. These rates have led to increased borrowing costs, reducing demand for goods and slowing down business investment in capital and inventory. The Federal Reserve's interest rate policies continue to influence the sector's performance, contributing to ongoing contraction (Reuters, Jul 1, 2024).

Supply Chain and Inventory Issues

The ISM report for August 2024 indicates that supplier deliveries are slowing while raw materials inventories are expanding. However, backlogs have dropped significantly, highlighting a mismatch between supply and demand. Manufacturers have reported challenges such as fluctuating customer orders, decreasing sales backlogs, and reduced production levels due to weak demand.

Purchasing Costs and Inflation

While inflation pressures have been easing, the manufacturing sector still faces challenges related to purchasing costs. Although the ISM report does not specifically mention a rise in purchasing costs for August, previous reports have highlighted the impact of inflation on manufacturing costs. The Prices Paid Index, which gauges the change in input prices, has shown some easing in inflation pressures but not necessarily translating to reduced purchasing costs for manufacturers (Reuters, Jul 1, 2024).

Summary of Latest ISM Report

The key findings from the latest ISM report include:

- Manufacturing PMI: 47.2 in August 2024, indicating contraction.

- New Orders: Contracting, with a significant slowdown in orders.

- Production: Contracting, reflecting weak demand.

- Employment: Contracting, suggesting a cautious approach to hiring.

- Supplier Deliveries: Slowing, which can indicate supply chain disruptions.

- Inventories: Raw materials inventories expanding, while backlogs are decreasing.

These indicators collectively paint a picture of a manufacturing sector facing significant challenges, including weak demand, economic uncertainty, and the impact of higher interest rates on purchasing costs and overall economic activity.

Interconnected Impacts on the Dow Jones Industrial Average (DJI)

The performance of the Dow Jones Industrial Average (DJI) offers insights into how these manufacturing challenges impact broader financial markets. As of August 30, 2024, the latest price for the DJI was 41,563.08. Over the past year, the index has seen a high of 41,585.21 and a low of 32,327.20. Despite the manufacturing sector's struggles, the DJI has returned 19.13% over the past 12 months. Its Sharpe ratio stands at 1.31 with an annualized standard deviation of 10.57%, indicating a favorable risk-adjusted return over this period.

This performance amidst manufacturing sector weaknesses can be attributed to several interconnected factors:

- Diversification: The DJI comprises various sectors beyond manufacturing, including technology and healthcare, which may offset manufacturing sector weaknesses.

- Investor Sentiment: Positive investor sentiment driven by hopes of economic recovery and strong corporate earnings reports from non-manufacturing sectors.

- Monetary Policy: While higher interest rates have affected manufacturing, they may benefit financial stocks within the DJI due to higher lending rates

Conclusion

The US manufacturing sector is currently facing several challenges, as highlighted by recent data and reports. Contracting manufacturing activity, slowing demand, higher interest rates, supply chain issues, and persistent purchasing costs are factors impacting the sector's performance. Despite these challenges, broader financial markets such as the Dow Jones Industrial Average have shown resilience due to diversification and positive investor sentiment.

The interconnected impacts of these factors highlight the complex nature of economic dynamics where weaknesses in one sector can be mitigated by strengths in others. Policymakers and industry stakeholders must navigate these challenges carefully to foster a more balanced economic recovery.

This document was created by Daizy using institutional-grade data and in collaboration with several external Large Language Models. All calculations were performed by the Daizy LLM Analytics Service. The contents of this document do not constitute investment, tax, or legal advice, and Daizy (Vesti.ai Ltd) is not authorized to give any advice. [Please refer to our terms of use.]

.png)

.png)